Because credits springing from fiat inflation provide an easy financial edge, they have the tendency to encourage reckless behavior by the chief executives. This is especially the case with managers of large corporations who have easy access to the capital markets. Their recklessness is often confused with innovativeness—Jörg Guido Hülsmann

In this issue:

Jollibee’s 2023 Record Sales and Income in the Lens of Consumer Health, Inflation and the Economy

I. Measuring Consumer Health: An Alternative View of Jollibee’s Record Sales

II. Q4 2023 Domestic Sales Growth Rate Fell to a 2.5-Year Low!

III. JFC Sales Slowed More than the Food Service GDP (Q4 and 2023)

IV. Slowing Sales Growth in the Face of Record Employment Rate and Historic Consumer Credit Growth? JFC’s Pacman Strategy Redux

V. As a Primary Beneficiary of the BSP’s Inflation, JFC Widened Margins Pushed Net Income to Record Highs

VI. Despite Lower Debt Levels, Higher Rates Increased JFC Debt Servicing Costs

VII. Rising PER and Increasing Free Float Share of the PSEi 30; Conclusion

Jollibee’s 2023 Record Sales and Income in the Lens of Consumer Health, Inflation and the Economy

Inflation and market concentration boosted Jollibee's 2023 record revenues and income despite the deterioration in consumer health.

I. Measuring Consumer Health: An Alternative View of Jollibee’s Record Sales

Malaya Business Insights, March 13: Jollibee Foods Corp. (JFC) grew its profit by 22.4 percent last year to P8.98 billion from P7.34 billion the prior year. Revenues rose 15.2 percent to P244.11 billion from P211.9 billion, over systemwide sales (SWS) of P345.32 billion, up 16.3 percent from P296.82 billion. “Our full year 2023 results reflect the strength of our execution and resiliency of our brands. We achieved an all-time high revenue of P244.1 billion, a 15.2 percent increase year-over-year which translated to a new record operating profit of P14.4 billion, up by 45 percent compared to full year 2022. Year-on-year, we improved gross profit and operating profit margins each by 120 basis points (bps), reinforced by our cost efficiency initiatives and our ability to control non-inventory-related costs,” said Ernesto Tanmantiong, Jollibee chief executive officer.

Based on the published financial performance of 2023, the Philippine economy has been flourishing, according to the headlines.

Jollibee's [PSE: JFC] record sales and income levels is an example.

Because JFC is the undisputed market leader in the domestic retail food industry, its health gives a vital insight into consumer conditions.

Figure 1

In 2023, international sales have anchored JFC's historic peso revenues of Php 244 billion. Because of the low base, JFC grew by 84% from the pre-pandemic high in 2019. [Figure 1, upper chart]

In contrast, 2023 domestic sales signified 17.4% above the same period. The firm's unprecedented total revenue was 35% above the former 2019 record.

JFC's domestic sales (15.9%) outgrew its international sales (13.7% YoY), but these numbers were down in the last two years: 20.3% in 2021, and 39.5% in 2022 for the local sales vis-a-vis 17.4%, and 35% for international sales.

In total, 2023's sales grew by 15.2%, lower than 38% in 2022 and 18.8% in 2021.

And so, a relative comparison of growth rates reveals JFC's tangible slowdown.

Nevertheless, JFC previously backed up the truck on globalization. It lavished on overseas capex and asset growth over the past years until the post-pandemic 2021-2023. [Figure 1, lower pane]

Yet, the company seemed to have recalibrated its business strategy.

Despite being designated as the "fastest-growing restaurant brand in the world," domestic sales continue to anchor its sales. The % share of domestic sales has been recovering marginally since 2020.

The lack of impact from their overseas investments may have prompted a shift in their directional or strategic approach.

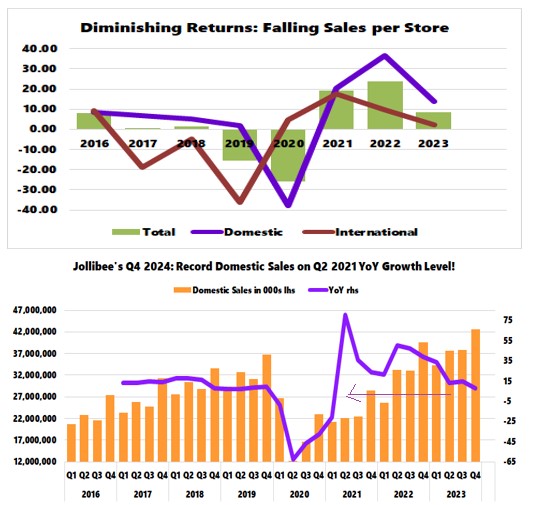

Figure 2

And despite the headlines, sales per store growth has been declining since 2021, with the cargo tilted towards overseas stores. [Figure 2, upper image]

Or, from the JFC's scorecard, domestic system-wide sales (SWS) growth slumped from 44.6% in 2022 to 17.6% in 2023, while overseas SWS fell from 34% to 14.4%.

Domestic same-store sales growth also plummeted from 40.6% in 2022 to 13.9% in 2023, while international identical store sales fell from 7% to 5.3%.

Store expansions and closure also provide some clues.

The JFC Group opened 658 new stores in 2023: 123 in the Philippines and 535 overseas (101 in China, 19 in NA and 40 in EMEAA. The JFC Group’s coffee and tea brands, SuperFoods, CBTL, and Milksha continued to drive the growth in store network with the opening of 192, 138 and 45 stores, respectively. A total of 225 stores were permanently closed in 2023: 69 in the Philippines and 156 abroad. (Jollibee, 2023)

The JFC Group opened 542 new stores in 2022: 123 in the Philippines and 419 overseas (86 in China, 25 in NA and 35 in EMEAA. CBTL, SuperFoods, and Milksha opened 103, 137 and 33 stores, respectively. A total of 259 stores were permanently closed in 2022: 58 in the Philippines and 201 abroad. (Jollibee, 2022)

Though more stores opened in 2023, the closure of more domestic stores in 2023 compared with 2022 further points to the weakness of Jollibee's main clients—the local mass market.

In a nutshell, signs of developing weakness have surfaced in JFC's domestic and overseas markets.

II. Q4 2023 Domestic Sales Growth Rate Fell to a 2.5-Year Low!

But there's more.

The firm's quarterly activities, its comparison to the economy, and the influence of inflation provide a more trenchant observation of its financial health.

Measured in quarterly performance, Q4 2023 domestic sales growth of 7.8% signified the lowest since the pandemic lockdown days of Q2 2021! [Figure 2, lower diagram]

And that was a period marked by holiday spending! Interestingly, the slowdown in quarterly sales growth emerged from Q2 2023. Incredible.

In essence, Q1's 34% growth delivered the gist of the 15.2% annual revenue increase. The sharply reduced growth rate in the succeeding quarters reinforced the downtrend of the annual topline growth.

III. JFC Sales Slowed More than the Food Service GDP (Q4 and 2023)

How did JFC's domestic sales growth perform relative to the sector's GDP?

Figure 3

Real food services GDP growth slowed from 18.5% in Q3 to 17.4% in Q4. It peaked in the reopening of Q2 2021 and has been southbound since. [Figure 3, upper diagram]

JFC's "real" or inflation-adjusted revenues may have grown by only 4.1% in Q4, lower than the 10.7% in Q3.

In annual terms, JFC's "real" revenue growth could be at 10% compared with the "real" 18.8% growth of the Food Services GDP in 2023. [Figure 3, lower graph]

The sharp difference between JFC's revenues and the Food Services GDP means that despite its unchallenged market leadership, SMEs grew substantially faster than JFC, or the gap may reflect an overstatement of the sector's GDP.

But this (Food GDP-JFC sales) chasm would hardly be the case since JFC's market leadership exhibits deepened market concentration.

In 2019, we discussed JFC's shift to a leveraged "Pacman Strategy,"

Firms with liberal access to credit can buy out competing firms, and therefore, result in the concentration of the industry. (Prudent Investor, 2019)

IV. Slowing Sales Growth in the Face of Record Employment Rate and Historic Consumer Credit Growth? JFC’s Pacman Strategy Redux

That isn't all.

Figure 4

Remember, the government bragged about the record-high employment rates last December (also Q4)? What happened to this labor windfall? [Figure 5, upper pane]

That's right. Jollibee's materially slowing quarterly sales, especially in Q4, dispute the alleged increased consumer spending capacity.

It strengthens our case about statistical anomalies or inaccuracies (deliberate or not).

The brisk growth rate or the historic increase in peso levels of consumer credit may have also been instrumental in JFC's unprecedented peso sales in 2023. [Figure 5, lower image]

Concisely, JFC's 2023 feat must have been a product of credit-financed deficit spending and aggressive growth in consumer credit rather than productivity improvements.

For this reason, inflation has played a substantial role in JFC's overall financial performance.

V. As a Primary Beneficiary of the BSP’s Inflation, JFC Widened Margins Pushed Net Income to Record Highs

With its predominant market position, JFC became a principal beneficiary of the BSP's monetary inflation—its profit margin soared along with inflation rates!

Figure 5

JFC benefitted either from its price pass-through effect on consumers or managed to control input costs through different channels ("cost efficiency initiatives and our ability to control non-inventory-related costs," shrinkflation, value deflation, etc.?) or from a combination thereof, resulting in its record profit (in pesos) despite the slowdown in its growth rate.

In 2023, profit margins widened to 18.9%, a hair breath away from 2017's pinnacle of 19%. [Figure 5, upper illustration]

Profit margins increased in the first wave of inflation in 2015-2017 and the recent second wave in 2020-23.

But even then, JFC's published net income grew by 22.4% in 2023, lower than the 38.4% in 2022—which may be a sign of struggling consumers. [Figure 5, lower chart]

Still, net income (in peso levels) was at an all-time high in 2023.

Or, JFC's record sales and income levels in 2023 were significantly boosted by inflation!

Given the backdrop of the softness of consumer spending, we await the publication of the annual reports to see how JFC's performance affected its smaller rivals.

VI. Despite Lower Debt Levels, Higher Rates Increased JFC Debt Servicing Costs

Figure 6

To be sure, after reaching a zenith in 2020, JFC has been reducing its debt level marginally. [Figure 6, upper window]

From 2020's pinnacle of Php 63.8 billion, it was down by 19% to Php 51.5 billion in 2023.

Despite that, the company's debt servicing cost continues to rise amidst rate hikes by the BSP (and the Fed—for FX debt). [Figure 6, lower visuals]

JFC proposes to raise Php 8 billion in preferred shares "mainly to refinance maturing obligations."

So, akin to other PSEi 30 issues, fund-raising has mainly been about refinancing existing debt, which subject firms to heightened interest rate volatility and risks.

VII. Rising PER and Increasing Free Float Share of the PSEi 30; Conclusion

Since its fall in 2019, market participants of the PSE have pumped JFC shares (end of the year) to raise its year-end price-earnings ratio, exhibiting price multiple expansion rather than improvements in "fundamentals." March 15th's close signified a 15.6 PER (2023 eps).

Figure 7

Trend-following activities have also pushed JFC's free float market cap higher to 3.55% at the close of 2023. It was 3.42% last Friday. JFC ranked 9th in the 30 elite members of the PSEi 30.

To sum up, the world's transition towards de-globalization and increasing focus on deficit spending elevates critical risk factors such as inflation, interest rates, etc., intensifying the fragility of a highly leveraged consumer-dependent environment. JFC's 2023 performance only validated these escalating vulnerabilities.

___

References:

Jollibee 17-A 2023 Annual Report, PSE.com.ph P.79

Jollibee 17-A 2022 Annual Report PSE.com.ph P.76

Prudent Investor Newsletters, Jollibee’s Fantastic Paradigm Shift: From Consumer Value to Aggressive Debt-Financed Pacman Strategy, March 3, 2019

No comments:

Post a Comment