Besides, stock prices are primarily information... they tell investors where their capital can be most fruitfully employed. The important thing is not that prices be high or low... but that they be honest—Bill Bonner

In this issue

The PSEi 30 in 2024: Debt-Fueled Expansion Amid Fiscal and Monetary Shifts

I. Monetary Tailwinds and a Fiscal Inflection

II. PSEi 30: Debt as the Primary Growth Driver

III. Record Revenues, Yet Slowing Growth Momentum

IV. Net Income Challenges: Slow Growth and Declining Margins

V. “Cui Bono?” — Who Benefits from GDP Growth? A Symptom of Trickle-Down Economics

VI. Sectoral Performance: Debt, Revenue, and Income Trends

VII Top Movers: Individual Firm Highlights

VIII. Final Notes on Transparency and Accuracy

The PSEi 30 in 2024: Debt-Fueled Expansion Amid Fiscal and Monetary Shifts

What the PSEi 30 tells us about the Philippine economy’s fiscal and financial direction in 2024.

I. Monetary Tailwinds and a Fiscal Inflection

The Bangko Sentral ng Pilipinas (BSP) initiated the first phase of its easing cycle in the second half of 2024, comprising three policy rate cuts alongside a reduction in the Reserve Requirement Ratio (RRR).

This coincided with an all-time high in public spending, bolstered by a surge in non-tax revenues. As a result, the Philippine fiscal deficit marginally narrowed to Php 1.506 trillion in 2024—still the fourth largest in history. To fund this gap, public debt rose to a historic high of Php 16.05 trillion.

Simultaneously, a steep decline in quarterly Consumer Price Index (CPI) readings during Q3 and Q4 pulled average annual inflation down from 6.0% in 2023 to 3.2% in 2024.

These three macroeconomic developments—monetary easing, record government expenditure, and easing inflation—served as key underpinnings of GDP growth. Despite noticeable slowdowns in Q3 (5.2%) and Q4 (5.3%), relatively stronger performances in Q1 (5.9%) and Q2 (6.5%) lifted full-year GDP growth to 5.7%, edging up from 5.5% in 2023.

Against this backdrop, how did the elite composite members of the PSEi 30 perform in 2024?

This article examines their financial performance, focusing on debt, revenue, net income, and sectoral contributions, while highlighting the broader implications for the Philippine economy.

Nota Bene:

PSEi 30 data include redundancies due to the inclusion of assets and liabilities of subsidiaries and their parent holding firms.

Chart Labels:

B 1A Recent Data: Consists of current members and includes possible data revisions from the past year.

1B Data: Reflects comparisons between previous years, consisting of members during the existing period and unaudited publications for the period.

II. PSEi 30: Debt as the Primary Growth Driver

Figure 1

In 2024, non-financial debt surged by 8.44% to a record Php 5.767 trillion, marking the third largest annual increase since 2018. (Figure 1, topmost pane)

This Php 449 billion net addition occurred despite elevated borrowing costs, with 10-year BVAL rates remaining high. (Figure 1, middle graph)

Relative to the broader financial system, non-financial debt accounted for 16.92% of total financial resources (bank and financial assets), slightly above the 16.87% share in 2023. (Figure 1, lowest image)

On top of this, the top three PSEi 30 banks reported a staggering 49.99% increase in bills payable—from Php 483.58 billion in 2023 to Php 725.30 billion in 2024. Notably, this figure excludes bond issuances.

III. Record Revenues, Yet Slowing Growth Momentum

Figure 2

The PSEi 30 collectively posted record revenues of Php 7.22 trillion, representing a 7.91% increase or Php 529.07 billion in absolute terms. This slightly surpassed the 7.8% growth or Php 478 billion gain in 2023. (Figure 2, upper chart)

However, in historical context, the 2024 increase ranked as the third smallest since 2018—reflecting the easing of price pressures as the CPI cooled.

Systemic leverage—defined here as the sum of public debt and universal/commercial bank loans (excluding fixed-income instruments and FDIs)—rose by 11.1% in 2024, reaching an all-time high of Php 29.96 trillion. (Figure 2, lower chart)

This expansion in credit, alongside continued deficit spending, substantially supported aggregate demand, thereby contributing to the PSEi 30’s revenue gains.

Figure 3

However, viewed from another lens, the slowing contribution of money supply relative to GDP—a key indicator of real economy liquidity—has increasingly revealed slack in both PSEi 30 performance and broader GDP growth. (Figure 3, upper image)

The 2020 spike in this metric underscored the BSP’s historic role in backstopping the banking system during the pandemic.

Yet it also marked a turning point in the financialization of the Philippine economy—an underlying force behind demand-side inflation and a structural driver of imbalances between financial sector gains and real-sector productivity.

Importantly, the deceleration in revenue growth mirrored the nominal GDP trends of 2023 and 2024, highlighting the interconnectedness of corporate performance and macroeconomic trends. (Figure 3, lower visual)

IV. Net Income Challenges: Slow Growth and Declining Margins

Figure 4

Net income across PSEi 30 firms grew at a sluggish 6.8% to a record Php 971 billion. While this represents a nominal gain of Php 80.31 billion, both the growth rate and the absolute increase were the smallest since 2021. (Figure 4, topmost image)

Despite widespread corporate participation in government projects, historic public spending growth of 11.04% outpaced net income growth, underscoring the accumulating inefficiencies in the effectiveness of 'trickle-down' policies. (Figure 4, middle graph)

The PSEi 30 maintained a steady net income margin of 13.44%, slightly lower than last year's 13.45% but still exceeding the 5-year average of 12.15% (2019–2024). (Figure 4, lowest chart)

Critically, the debt-to-net income ratio revealed that Php 0.46 in debt was needed to generate every Php 1 in profit.

More alarmingly, on a net basis, Php 7.3 in new debt was required for every Php 1 increase in profit—a record high.

The takeaway: Deepening debt dependency to drive profits is not only artificial but also subject to diminishing returns.

V. “Cui Bono?” — Who Benefits from GDP Growth? A Symptom of Trickle-Down Economics

Figure 5

Revenue as a share of GDP edged up to 27.3% in 2024 from 27.22% in 2023—marking the third-highest level since 2019. (Figure 5 upper window)

The PSEi 30 accounted for more than a quarter of nominal GDP, excluding additional contributions from other publicly listed firms under elite conglomerate umbrellas.

This substantial contribution highlights a hallmark of the government and BSP’s “trickle-down” economic development model, characterized by increased business operations through direct state spending, which disproportionately benefits politically connected corporate giants.

Importantly, the BSP’s easy-money regime functions as an implicit subsidy, enabling elite firms to acquire cheaper credit as a protective moat against competition.

The result: a centralization of economic gains among the elite, while MSMEs and average Filipinos—Pedro and Maria—bear the costs.

In essence, the model privatizes profits while socializing costs, exacerbating economic inequality.

VI. Sectoral Performance: Debt, Revenue, and Income Trends

In 2024, sectoral performance varied significantly: (Figure 5, lower table)

Debt: The industrial sector posted the largest percentage increase in debt at 17.33% year-on-year (YoY), but holding firms dominated in peso terms, accounting for a 67.85% share of total debt.

Revenues: Despite rising vacancies, the property sector recorded the highest percentage revenue gain at 16.6% YoY. However, holding firms led in absolute peso increases and percentage share, contributing 45.9% of total revenue growth.

Net Income: The services and property sectors outperformed with net income growth of 20.6% and 17.6%, respectively. Banks, however, led in peso growth and accounted for 45.6% of the net income increase.

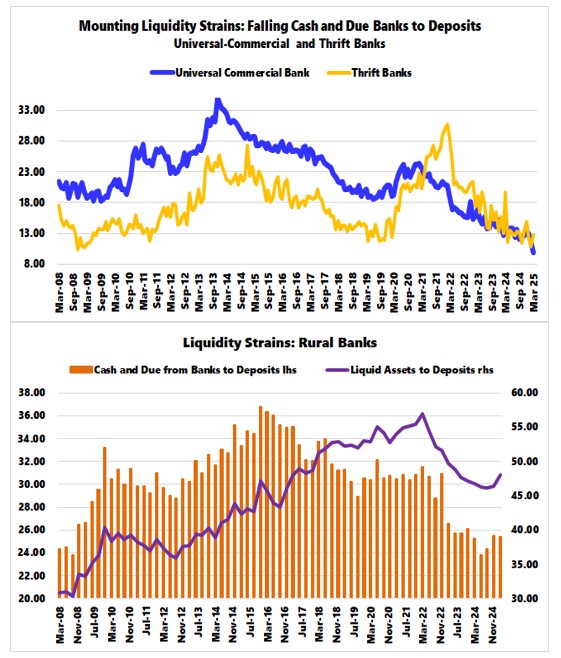

Cash Holdings: Non-financial firms’ cash holdings contracted by 1.91%, driven by a 14.6% and 3.35% decline in reserves in the industrial and service sectors, respectively.

In contrast, PSEi 30 banks saw their cash holdings rise by 14.6%, despite the BSP reporting otherwise. This discrepancy raises questions over possible dual standards in bank reporting.

VII Top Movers: Individual Firm Highlights

Figure/Table 6

Debt: San Miguel Corporation (SMC) led all firms with a Php 155 billion increase in debt, bringing its total to a historic Php 1.560 TRILLION—comprising 35% of all non-financial PSEi 30 debt. Ayala Corporation and its energy subsidiary ACEN followed with Php 76.9 billion and Php 54 billion increases, respectively.

Revenues: San Miguel, BPI, and BDO were the top contributors in terms of revenue increases. Conversely, DMC and its subsidiary Semirara reported revenue contractions.

Net Income: ICT, BPI, and BDO led net income growth in absolute terms, while SMC and SCC posted the largest declines.

Cash Holdings: The largest cash increases came from SMC and ICT, while Aboitiz Equity Ventures and LTG Group reported the steepest reductions.

VIII. Final Notes on Transparency and Accuracy

The credibility of this analysis rests on disclosures from the Philippine Stock Exchange and related official sources. However, questions persist regarding the possible underreporting of debt and the inflation of both top-line and bottom-line figures by certain firms.

Moreover, when authorities overlook or fail to act on instances of misreporting—especially by large, elite-aligned corporations—this raises serious governance concerns. Such inaction fosters moral hazard and risks entrenching a culture of non-transparency within the corporate sector.